Insights

Insights

In the midst of the data revolution, governments have amassed substantial data reservoirs. The metamorphosis of these data reservoirs into digital assets, akin to land and mineral resources, is emerging as a pivotal avenue for local governments delving into fiscal transformation. In August 2023, the Ministry of Finance promulgated the "Provisional Regulations on the Accounting Treatment of Enterprise Data Resources" (hereinafter referred to as the "Provisional Regulations"), which delineate the incorporation of digital assets into the balance sheet, slated for implementation commencing January 1, 2024. With the operationalization of "digital assets inclusion in the balance sheet," digital assets can serve as novel collateral for asset financing, bolstering urban investment assets while expanding financing avenues.

I.Conceptualization of digital assets

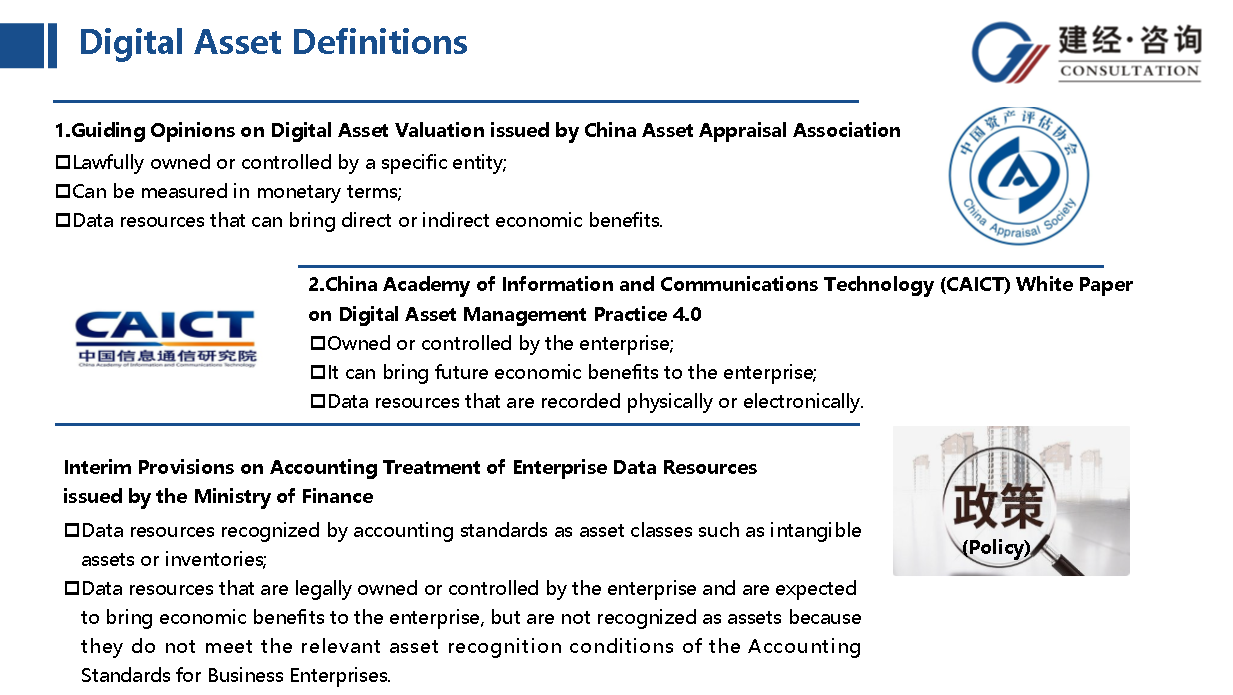

Prominent industry institutions have endeavored to define digital assets, with the "Provisional Regulations" from the Ministry of Finance furnishing stipulations for the recognition of enterprise digital assets. Succinctly put, digital assets denote data resources capable of generating value for an enterprise. For data to attain the status of a digital assets, it must satisfy at least three fundamental conditions: ① stemming from past transactions or events of the enterprise; ② owned or controlled by the enterprise; ③ anticipated to yield economic benefits for the enterprise.

Based on the diverse origins of data, digital assets can generally be categorized into three types: personal data, public data, and enterprise data. Their salient characteristics encompass intangibility, interdependence, diversity, variable worth, and manipulability.

II.Recognition of digital assets

The conversion of data from a resource into an asset and subsequently into capital necessitates adherence to the following criteria:

①Possession of data resources with applicable scenarios and foreseeable economic benefits;

②Definite ownership of data resources, enabling valuation through rational methodologies, facilitating their incorporation into the balance sheet as assets;

③Existence of a trading platform or financing monetization mechanism.

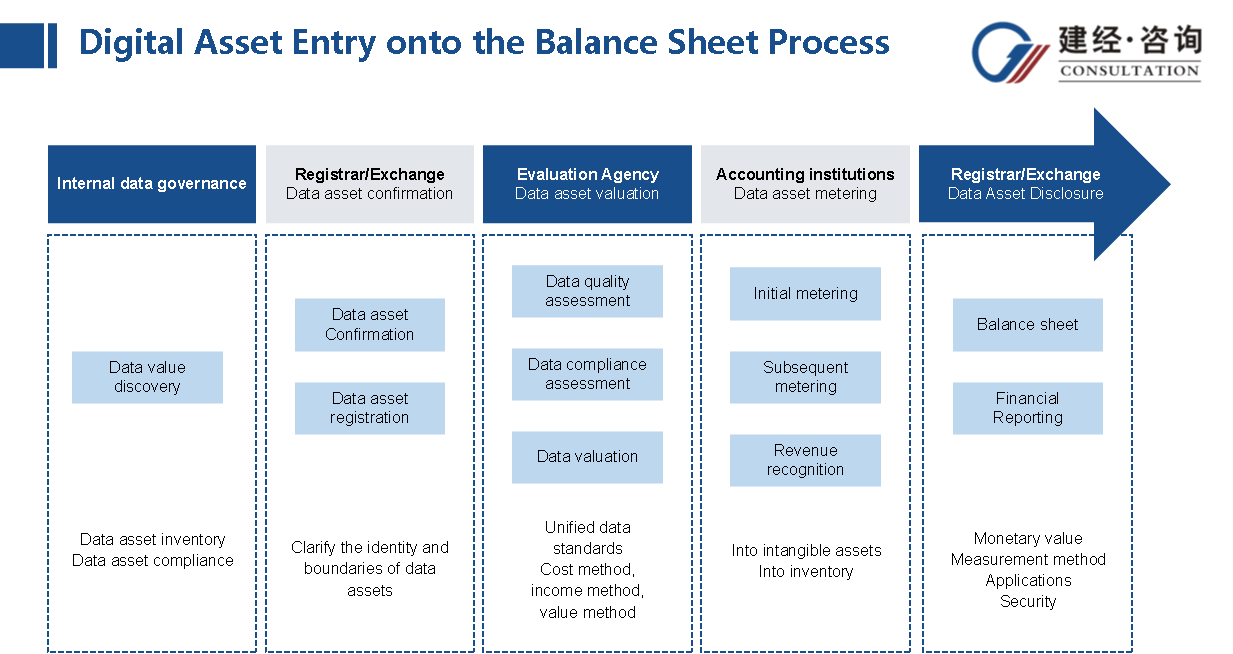

The confirmation of data property rights constitutes the pivotal juncture in the digital assetsization process. In China, the "Data Twenty Policies" were introduced to address the issue of data property rights, advocating a framework for data property rights system delineating the separation of data resource ownership rights, data processing usage rights, and data product operation rights. In practice, this framework primarily unfolds through data exchanges, wherein enterprises submit applications for data property rights to the exchange. Following verification and review, the exchange issues data property registration certificates to effectuate data property rights confirmation.

The "Provisional Regulations" enable the accounting treatment of digital assets within the balance sheet, recognizing data as an integral component of the "assets" item within the enterprise's balance sheet, thereby reflecting its actual value and business contributions in financial statements. This process entails several procedural steps such as digital assets recognition, digital assets valuation, digital assets quantification, and digital assets disclosure. The inclusion of digital assets in the balance sheet furnishes legal foundations and streamlines operational procedures for the transition of data resources into digital assets.

III.Valuation of digital assets

Concerning the valuation of digital assets worth, the China Appraisal Society's "Guidelines for digital assets Valuation" delineate provisions on valuation subjects, operational requisites, evaluation methodologies, and disclosure mandates. It identifies three fundamental methods and their derivatives for appraising digital assets value: the income approach, the cost approach, and the market approach. Initially, the "Provisional Regulations" endorse the cost approach for balance sheet inclusion. As the marketization of digital assets matures, adoption of either the market approach or the income approach for evaluation during subsequent asset-backed financing becomes feasible.

IV.Instances of digital assetsization

Presently, digital assetsization, inclusive of balance sheet inclusion, predominantly transpires within the domain of enterprise data. For public data, various levels of government confer free authorization to regional state-owned big data entities or state-owned urban investment firms for operation, colloquially termed as the first-tier developers of data. Typically, first-tier developers in the public data sector preprocess government-sanctioned public data through organization, cleansing, and anonymization, ensuring data integrity under the tenet of 'utilizing data without divulging data,' enticing second-tier developers from diverse industries such as healthcare, finance, and education to formulate multifarious application scenarios. While upholding conditional free usage of public data for purposes of public governance and public welfare, relevant stakeholders can undertake reasonable measures to garner returns. Concurrently, state-owned first-tier developers can leverage public data for asset appreciation, rate them, and subsequently engage in external financing through bond issuance and loans, operating analogously to traditional urban investment firms.

Data constituents constitute pivotal production resource factors for future economic progress, with public data constituting an integral facet of data resources influencing all facets of national economic advancement. They encapsulate substantial socio-economic value, underscoring the significance of their development, utilization, and market-oriented allocation. The introduction of pertinent policies has proffered clearer and more standardized directives for digital assetsization operations, furnishing local governments with a novel asset financing modality. Nevertheless, during the assetization process, meticulous attention must be directed towards the security and accuracy of public data. Local governments must delineate the ambit of public data usage to monetize public data in a legal and compliant manner.

We will contact you within 24 hours.

EN

EN